Embracing The Money Printers

Overview

This post looks at:

How you can make wealth even if your rental property doesn’t go up in value and if you don’t pay down your mortgage

How inflation can aid you

Inflation

My worldview lens is typically biased against the Slavery System as it is inherently evil.

The Slavery System is the term that I use to define all of the systems in place to extract value from the serfs of the world, feeding it up to their overlords.

One of the main tools of the Slavery System is Inflation. A deliberate mechanism carried out by governments to silently steal from you.

Rebalancing

I was recently looking at rebalancing investments away from Real Estate. Not fully, but turning down the volume.

What would I move it into?

Probably Gold.

I don’t see any growth with my local market for another decade and governments find things attached to the ground quite easy to extort.

However - as your wealth increases it is important to maintain orthogonal separate investments for diversification.

The reason for this is to avoid the heavy asymmetry experienced with drawdowns. 50% down means to get 100% to get back where you started. A dilemma if you don’t have any asymmetric investments.

So my gut feeling was to buy more Gold.

However, before doing that - let us examine something that is easy to overlook and forget about Real Estate. Debt Debasement.

I believe we are moving towards higher inflation, so I should take that into consideration.

Debt Debasement

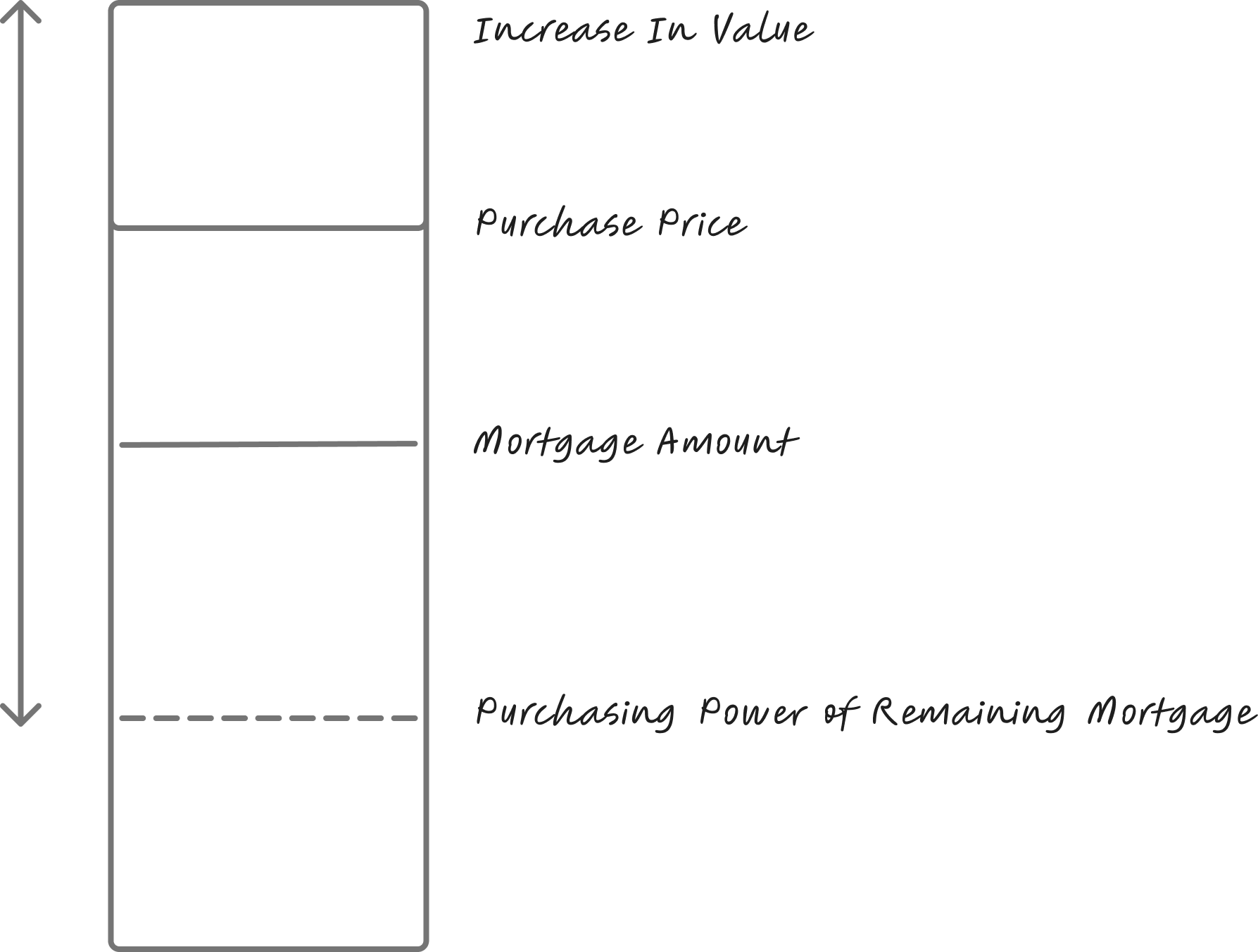

You make money when your asset goes up.

You also effectively make money when the debt you owe goes down in purchasing power. The delta between our debt’s purchasing power and any increase in real estate is your wealth increase.

So for example if you owed some money over 25 years and paid it back on the last day. If the Inflation Rate was 3% - You’d effectively be paying only half of it back. And if it was 10% inflation for 25 years, you’d be paying back less than 10% of what you borrowed.

3% - 52.2% reduction

5% - 70.5% reduction

8% - 85.4% reduction

10% - 90.8% reduction

Which Inflation Rate To Use?

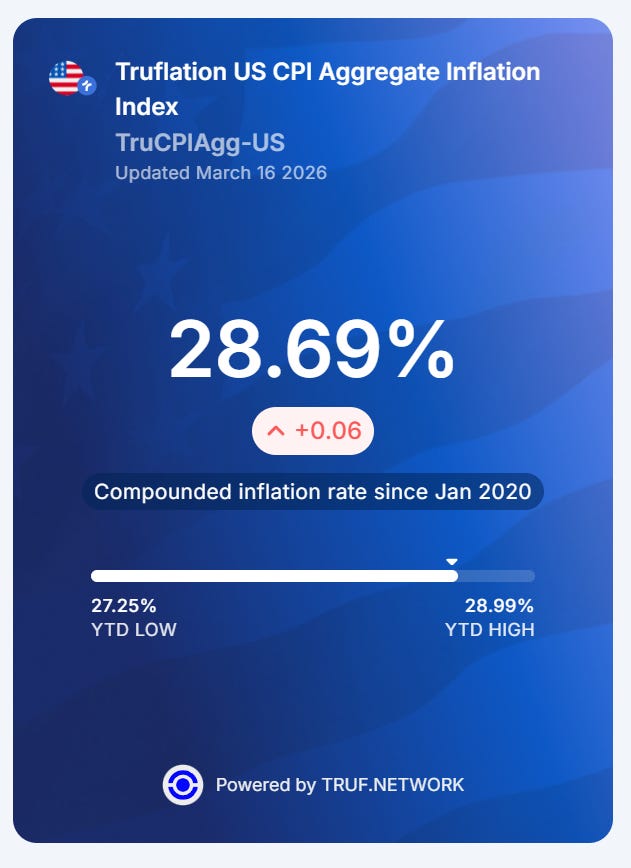

CPI is a well known lie. Manipulated by Government to hide the secret stealing power of money printing.

I’ll use an alternative source - Trueflation Index - Truflation provides real-time CPI, inflation components, and macro indicators derived from transparent, unbiased data sources.

They keep their numbers closely held to their chests but we can backfill their geometric mean numbers.

This is equal to 4.1% CAGR for that time period.

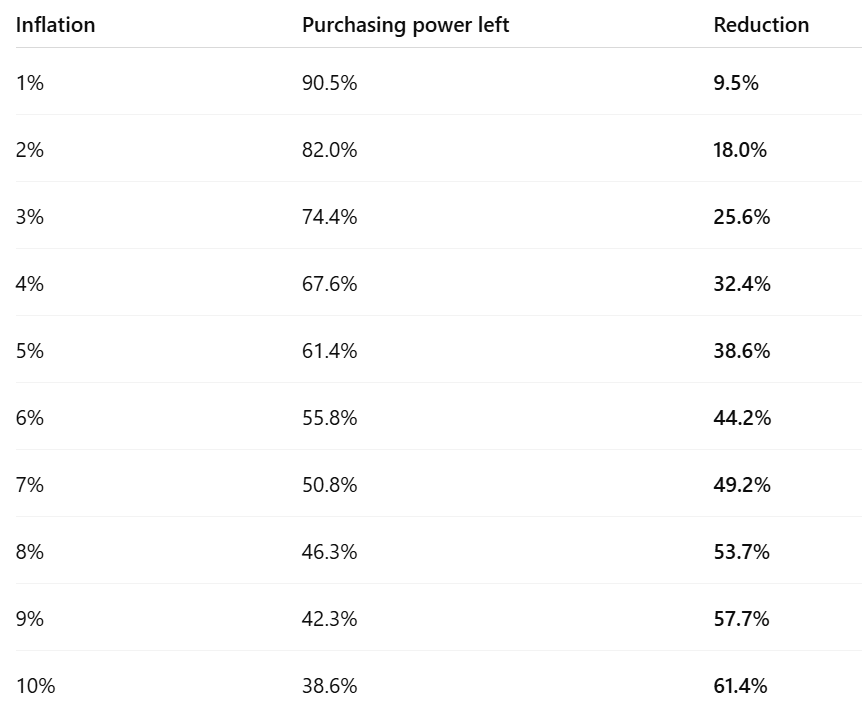

So for a 10 year period at various inflation levels you can see the debt debasement impact below.

I believe that the next 20 years will be much higher inflation than seen before - I believe much greater than 5%.

But if we take 5% as a round number, over 10 years, the purchasing power of your debt will have been erased by almost half - just shy of 40%. Or said another way the amount of stuff you can buy with that money that you owe has been greatly reduced.

So even if our house didn’t go up in price and even if we didn’t pay down the mortgage, we’d still be up by ~40% over the 10 years.

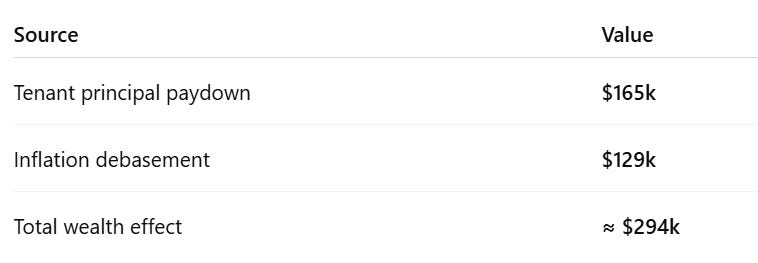

If we also factor in the tenant paydown on a purchase price of $625k ($500k mortgage and $125k down payment) and a 5% mortgage interest rate.

So roughly a 13% per year return. If the value of the property goes up then so also does the return.

Obviously if the inflation goes up so does that total wealth effect to you.

We can see from the numbers that a good portion of that wealth increase comes from the Inflation Debasement.

Summary

In summary, I believe inflation is going up.

It is important to remember that inflation can help you by eroding the purchasing power of that debt.

Keep in mind during these strange times, whenever there is a liquidity crunch, Banks can ask for the full debt to be repaid at any point. Also during these times interest rates can increase.

So be very mindful of cash management, liquidity and being over levered.