2025 Annual - Wealth Growth Update (Part 1)

📈 -5.65% Yearly Return / ⬆️ 23.53 % 9 Year CAGR / ✔️ Doubling 3.06 Years

To start off a little background listening - because - why not?

Well Well Well - a negative return - it happens! The doubling point is still pretty close to every 3 years.

I hold ~12% of my wealth in the Stock Market.

We’re focused on aiming for sub 3 years - as this is our doubling point. Our money doubles every 3 years.

Last year’s return was 80.79% so it all balances out.

I don’t count house or personal possessions in my net worth.

Our title last year -

Raking Back Wealth

I don’t contribute to investments anymore and I haven’t done for a few years. Once I figured out that I had enough invested to hit where I wanted to be at an older age I figured it made more sense to focus on “raking back” quality of life from the future to now. (COAST FI)

I didn’t want to be a Trillionaire at age 80. I’d rather be an extremely-well-lived centi-millionaire.

Keep in mind - we’re all different. And even I was different to me of 10 and 20 years ago. What drove me 10 years ago is different to what drives me now.

10 and 20 years ago it was all about numerical wealth. Now it is freedom then moving back to wealth accumulation.

Change in Income

I really wanted to work from home (or anywhere in the world) to maximize freedom so I really focused on finding a job that would allow me to to work from anywhere. I wanted to experience it and see what it would be like being able to move to different locations and work from there for a few months.

I’ve really enjoyed being able to exercise at lunch as well as help the kids out as/when they needed me. This has definitely been a great step towards freedom.

The idea of driving down town with millions of others to end up in a soulless gray cubicle makes my blood boil at the idea.

Having this extra freedom meant my income dropped quite a bit, but I’m OK with that for the quality of life.

Finding these remote jobs is pretty hard nowadays. Post Covid the sheep thinking of management was to pull everyone back into the building so they can collaborate and enjoy the culture.

I for one, experienced working from home during Covid and would find it extremely difficult to go back.

Horses for Courses

An old fashioned English saying -

Horses for courses

such as - you may want to ride a different horse for a different course.

There are two variables in life. Money and Time. They are interchangeable. When you are born you have more time than money and when you die - you have more money than time.

At some point in the value shifts from one to another. This for me, hit precisely around mid-life. Now time is more valuable than money.

Time is also analogous to the economic term of Time Preference - or how much value you place on living now than some future date.

For me mid-life coupled with Covid coupled with introduced risk of the the End of the Long Term Debt Cycle (Globally) meant my preferences pivoted.

Disconnect With Reading Materials

I started bumping into a disconnect between how I was feeling and what I was reading. I’d read one thing and feel a disconnect, it didn’t sit well with me.

Remember - there are two contexts. Time, Money.

Most financial reading and YouTubers will sit in the context of Money (i.e. all guidance is aligned with getting you the maximum amount of money). It will be written to mathematically give you the best return. Such as stick it in a tax deferred account because it will probabilistically give you a better return. Or do this or that with your money because it provides the best Tax Protection.

However - this blindly shuts out anyone who values freedoms or one could say those with a bias towards Time preference. Having your money locked away until you are 65 isn’t Freedom and it isn’t Time oriented. Having constraints around my wealth is not Freedom enabling and this is what has been bugging me about financial education.

I’ve remarked on the difference between Speculator and Investor recently. I’m feeling a draw towards the Investor aspect recently - the want to have cashflow as a priority and as a Freedom enabler rather than a later in life option. I do fully aim to flip back to growth mode once I have hit a comfortable freedom point.

The Small And Mighty Real Estate Investor

I remember being a huge fan of alternative music when I was younger as well as playing computer games.

Generally speaking - NO ONE DID THIS. People would make fun of me, how I dressed, what I listened to, what i did with my time. This went on for decades.

Luckily, early on I realized that I should never care about what people thought about me.

However - I’d always be looking for some sort of confirmation of others doing the same. Seeing that acknowledgement that it OK to be doing what you are doing is some innate human want. The minute you see it - you double down and go harder on whatever weird thing you are doing.

Well I feel the same way about the way I see finance.

What I’ve realized is that opinion that I receive comes from - People who want to stay inside the Matrix (or are unaware of being part of the Matrix).

Or said another way - they don’t have the same strong opinions on Freedom as I do. And they likely in the same Time preference as I am.

The idea of paying down rental mortgages to have cash flowing assets is alien to them. The idea of having investments outside of deferred Tax mechanisms is also alien.

They are seeing the world from a Money point of view. I’m now seeing the world from a Time point of view.

I was reading The Small and Mighty Real Estate Investor and walked past an approach that Chad Carson called “Ending”. His book points out that things don’t need to be in a linear fashion. Such as the canonical build wealth, retire, die.

He writes that things can be done in phases, building and leverage then perhaps de-risking by paying down a property and securing some income. And then maybe perhaps going back to the building phase again.

Reading this resonated with me. This is what I want to do and it having someone call it out in a book makes me feel less crazy for wanting this.

If I pay off one of my rentals, I’ll get an immediate 20% return on my cash per year going forward. This is a step towards swapping out earned income with an alternative cash flow source.

Plotting the course towards Time preference.

Bigger Buys

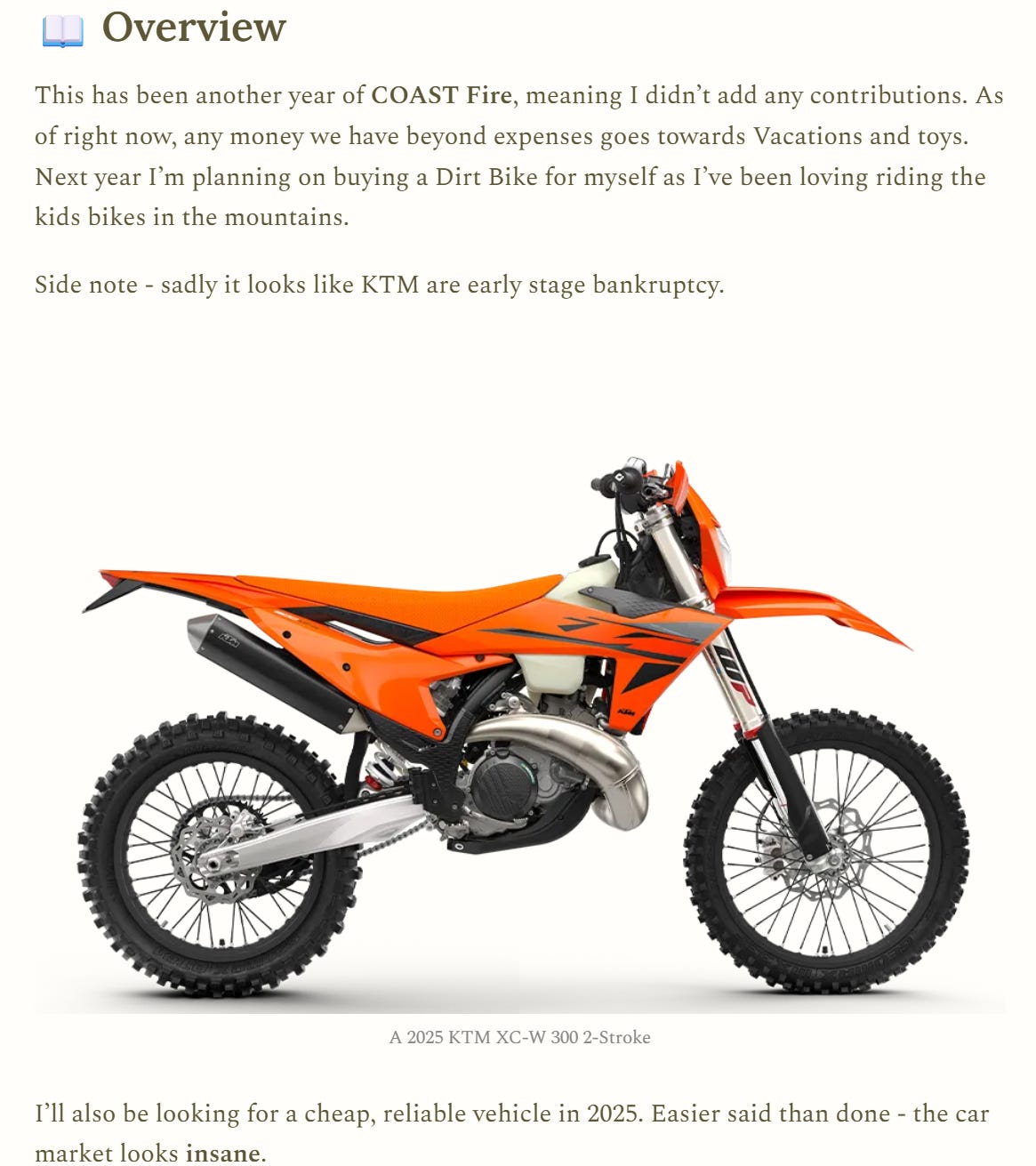

Part of the drop of assets is down to me buying a $40,000 SUV cash, a $10k KTM Dirt Bike and a fairly expensive Bullion Scanner.

It looks like I did what I said I was going to do last year - so that’s good!

The bike has brought me so much joy. The vehicle extends the runway for us to drive around to jobs, maintaining our income.

Excerpt from last years end-of-year review:

The Good, The Bad, The Ugly

The Good - Bullion.

I’ve been talking about Bullion since I started writing in early 2024. Yes; Gold Bugs have been talking about it since it became an element. But for me there were better investment opportunities at the time.

I had put 2.5% of Net Worth into Gold and Silver early 2024. I look at investment moves in percentages. 1, 2.5, 5 or 10%.

I had a previous small position of Silver. After that I moved into buying Gold and Silver stocks in my equities accounts.

Since then the price of Gold and Silver has doubled and Silver is gaining a lot of momentum. So yea - over 100% return on all of those investments. Some of the stocks were a lot more. As I previously mentioned, unless the investment is a unicorn, I typically sell 100% of my buy in amount so that the returns are infinite.

The chart above is one of importance. Everything reverts to the mean (average). You can see from this chart that the ratio between Gold and Silver (gold and silver ratio) is now, visually, landing smack center of a ~25 year average. Implying that the sky rocketing Silver prices will slow down relative to Gold.

Now I know that the Gold/Silver ratio was in ancient times a lot closer to single digits rather than in the 50s. My understanding that from a pure metals in the ground point of view, Silver is roughly 10 to 1 in there with gold.

I can imagine a bit more room for silver to gold repricing however, logically, I would imagine Silver to peg itself to the gold price and rise relative to Gold soon.

The LBMA and COMEX’s long running paper market manipulation is becoming less and less relevant and China seems to be taking over as the true spot price. There has been a recent price discrepancy between East and West with prices being higher in the East. Any delta becomes a target for arbitrage.

I think Gold and Silver will continue to rise in 2026, 2027. I think there are so many leftfield factors that could affect the price including: BRICS, Russia/NATO, End of Fiat and so on that the numbers could really jump.

The Bad - Stock Market

I “correctly” sold all of my stocks like literally the day before they dropped a million percent. HOWEVER - timing the market is not a thing and should not be done. I think having an opinion on where something is going at a Macro level makes sense, but timing it - that’s tough.

I shouldn’t have exited to cash. I’m not saying being in the stock market during 2025 was bad, just that I shouldn’t have exited to Cash.

I’ve seen statements about Buffet say being heavily cash, however I now realize that the reason he is heavily cash is that he is playing in a different game, where he can only invest in certain investment vehicles. Where an individual investor can invest really in anything.

2025 Me regrets being in ANY Tax Deferred accounts for the inability to move cash around to wherever and whatever I choose.

I’ve now changed my internal rule set for Capital Allocation to never be cash.

Yes the Stock Market is up a ton this year and yes I think it will continue to go up. However as per my previous posts - I believe this to be the work of mal-investment.

Would I swap my investments outside of the stock market kind-for-kind with more shares in the stock market? Never.

We have just re-entered quantative easing round (5/6/7 not sure which) meaning that more dollars go into circulation, slowly pumping up all assets. I think quantative easing, global trust of the United States Dollar mean that as I’ve mentioned before - the USD will go up like a firework, outpacing everything - then pop.

This Chief Investment Officers take on 2025 is an interesting watch as an alternate opinion to mine.

He highlighted the Canadian Stock Markets return being quite excellent during 2025.

However with a straight face, he states that he wouldn’t recommend Bitcoin or Bullion in one’s holdings.

Looking at the holdings of the Canadian Stock Market - S&P TSX - unsurprisingly a good chunk of it is Mining. The other large chunk is banks. I’m morally against banks. Mining I’ve already got a lot of - just mainly hedged to the USD.

I think of 3 variables when I think of life. Time, money, and freedom. You can have a lot of time and money, but without freedom, your quality of life is very poor.

Freedom is your ability to exercise free will to decide what to to with both your time and money, and is measured by the level of dependence you have to people and systems.

Like you pointed out, you have very little freedom when your chained to a corporate job, but you also don't have very much freedom when you are a baby (with the most amount of time you will ever have) or when you are old and infeeble (and likely when you will have the most amount of money you will ever have).

That's why an equally important investment, more so now than ever, are relationships grounded in love, dignity, and respect, because good parents give their children as much freedom as they can safely manage when they are babies, and well raised children do likewise with their parents when they are old.

Being a millionaire in your 70s doesn't matter much when you are in an assisted living center, alone, unloved, unable to care for yourself, and at the mercy of people with no emotional attachment to your well being.

That is when a deficit in freedom really becomes apparent.